Improving the looks of your house and making minor or major changes to your house is always very satisfying but entails a lot of expenditure. Perhaps you have always wanted to give your home a facelift but you are worried about the cost; home equity could be the answer.

Borrowing money against the value of your home allows homeowners to facilitate the renovation of their homes without the pressure that comes with expensive services. Now, let’s consider ways of realizing your home makeover visions with equity access and contemplating the varieties of financing.

Understanding Home Equity

Before going any further in explaining the home equity mortgages and loans it is important to establish the concept of home equity. Home equity can therefore be defined as the current value of your home minus the amount that is owed on the mortgage.

It is that part of your property that you can consider yours since you maintain full control over it. For instance, your home is worth $400,000, while your mortgage balance is $ 250,000; thus, your home equity is $ 150,000.

In 2023, the average Idaho HELOC balance grew 2.7% to $42,139, and more than $20 billion was added to the total HELOC debt across all U.S. consumers. This means that people in Idaho support HELOC to have a home for themselves and family.

This equity is a part of Idaho heloc and may then be utilized, especially as security for getting loans or lines of credit to finance home improvements, debt management, or any other large costs. Home equity can be tapped in three major ways and these include; the home equity mortgage, home equity loan, and the home equity line of credit or HELOC.

What is a Home Equity Mortgage?

A home equity mortgage, which is essentially a second mortgage, enables a homeowner to borrow money against the value of his/her home. This kind of credit operates in the same way as regular credit and is commonly an additional credit to the primary mortgage.

Money acquired through a home equity mortgage, among other things, can be used for home remodeling, children’s education, or paying off debts.

Advantages of a Home Equity Mortgage

- Lower Interest Rates: The benefit of home equity is often the lower interest rate than in the case of a personal loan or credit card since the mortgage is secured by the house.

- Tax Benefits: Often the interest given on a home equity mortgage is tax deductible, so it is a cheap source of funding.

- Flexible Use of Funds: You are free to spend the money you get from the home equity mortgage on anything you want to, as the money is yours.

Disadvantages of a Home Equity Mortgage

- Risk of Foreclosure: If one defaults in paying for the home equity mortgage, the home that he offered as a security can be repossessed.

- Additional Debt: This form of credit increases the level of indebtedness that you have to manage together with your first mortgage on a home.

Home Equity Loan vs. Mortgage

As for the further decision-making process about home equity tapping, you may encounter a home equity loan vs. mortgage dilemma. As much as these two materials appear to be almost similar, they have a few distinctions to make.

Home Equity Loan

A home equity loan is a non-recourse loan in the form of a lump sum that has to be paid off in the set time with agreed monthly installments. Also known as a second mortgage, it should not be confused with a home equity mortgage though it is equally a mortgage.

Mortgage

A conventional mortgage is financing to acquire a home, and it is the foremost lien on the home in most cases. A mortgage is a type of financial scheme in which an amount is lent for purchasing a home and is repaid gradually for a specified number of years like 15, 20, and 30 years, and the home acts as security for the loan.

Comparing the Two

- Purpose: A home equity loan is more or a line of credit that is taken to meet specific purposes such as home improvement or payment of other expenses whilst a mortgage is intended for the purchase of a dwelling.

- Loan Amount: Home equity loans are based on the equity the home and the borrower has in the house while mortgages are taken based on the cost of the house.

- Repayment Terms: Both have a fixed date through which they are to be paid, but the length of the date may vary as well as the interest rates of each of the credit types: home equity loan and the original mortgage.

Mortgage vs. Home Equity Loan: Which is Right for You?

This paper aims to determine the suitability of taking a mortgage or a home equity loan depending on specific factors. Here are some factors to consider:

When to Choose a Home Equity Loan

- Home Improvement Projects: Whereas, if the borrower is interested in getting funds for certain home improvements, then a home equity loan will help him get a lump sum amount that will be enough for the required purpose.

- Debt Consolidation: High-interest debts can be consolidated using the home equity loan which can, in turn, allow you to pay off that particular loan at a lower interest rate.

- Fixed Payments: Fixed interest rate along with the payment schedule is also an advantage of home equity loans particularly when it comes to monthly payments.

When to Choose a Mortgage

- Home Purchase: A conventional mortgage is suitable if one is purchasing a new home.

- Lower Interest Rates: In case you get a new mortgage that attracts a lower interest rate than the one on your current mortgage, then consolidating your existing mortgage would make sense.

- Long-Term Planning: If you intend to live in your house for many years, fixed-rate mortgages which have long-term installments prove to be useful.

Home Equity Line of Credit (HELOC)

The other possibility to get your home equity is the Home Equity Line of Credit also known as HELC. A HELOC is different from a home equity loan in that a HELOC is an open line of credit that works like a credit card whereby a homeowner borrows only what he needs and up to the limit for as long as the credit is active.

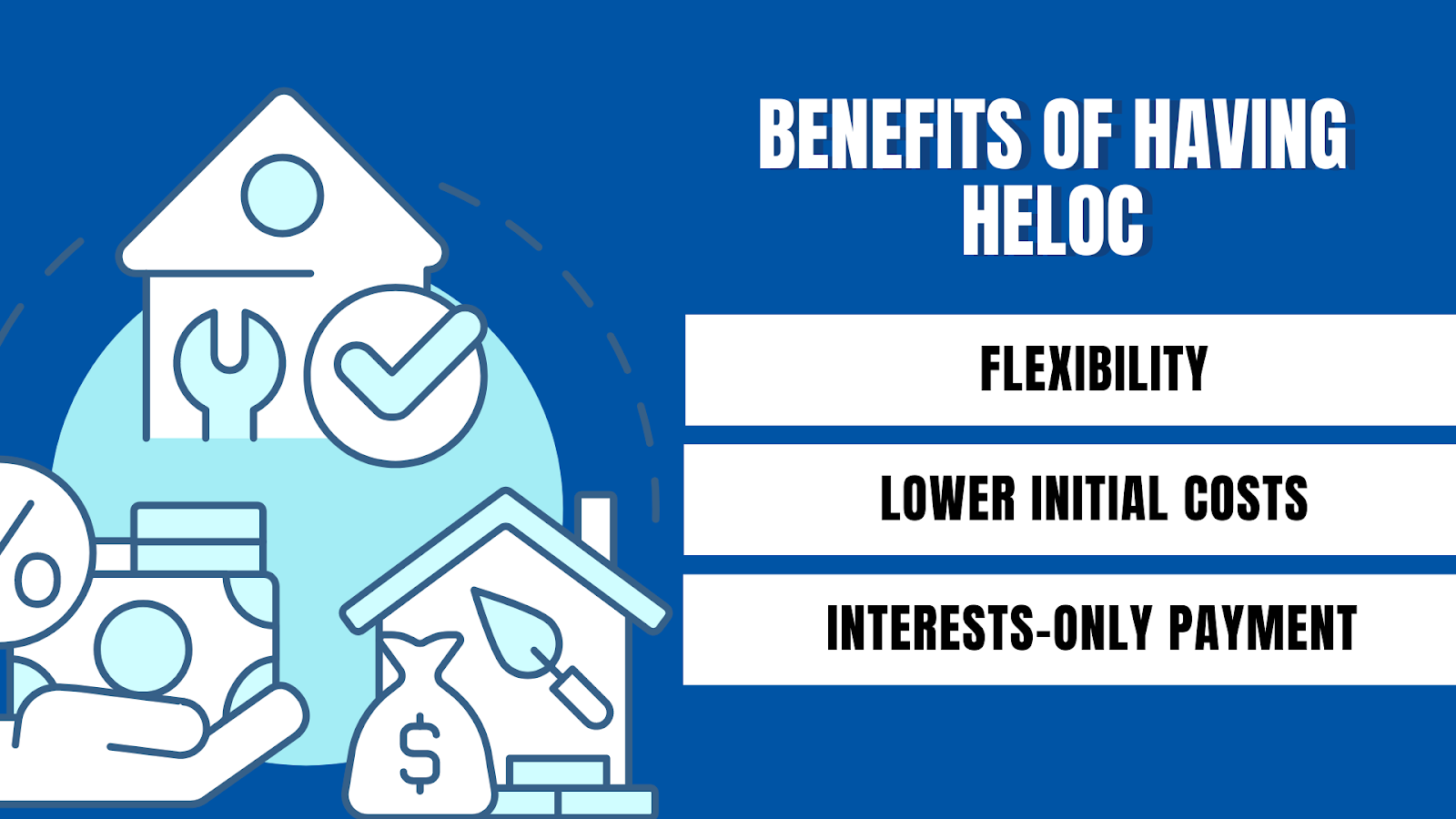

Benefits of a HELOC

- Flexibility: The amount of money you can borrow to fund is not restricted and can range from very small to very large hence suitable for projects with fluctuating costs.

- Lower Initial Costs: Specifically, one should note that HELOCs are generally cheaper in terms of the initial costs compared to home equity loans.

- Interest-Only Payments: The money is perhaps very easy to access and during the draw period, one can even start to make interest-only payments for ease of cash flow.

Drawbacks of a HELOC

- Variable Interest Rates: Some HELOCs come with variable interest rates and this, for most applicants, means that the rates cannot remain fixed.

- Potential for Overspending: This is one of the biggest drawbacks of having a HELOC because the availability of a line of credit, creates room for spending that is beyond one’s ability to pay.

- Collateral Risk: Other than these, your home is used as security, meaning that should you be unable to make your payments, your home can be repossessed.

Making the Decision

It is therefore important to factor in one’s circumstance, objective, and the construction and remodeling needs of the makeover project when deciding the applicability of the home equity mortgage, home equity loan, or home equity line of credit. Here are some steps to help guide your decision:

- Assess Your Equity: To begin with, it is recommended to know how much of an equity one has in the home. It must be noted that this is the maximum loan amount you can be approved for, the actual amount that you may be deemed to qualify for will depend on several factors that the loan officers consider when approving the loans.

- Evaluate Your Needs: Think about the range and expense of your home transformation work. Do you want to finance a large remodeling project or common repairs and improvements? It is also necessary to identify the total amount of the given and anticipated costs to compare different funding opportunities.

- Compare Interest Rates and Terms: Check and compare interest rates and all terms that concern home equity mortgages, home equity loans, and HELCOs. Make it a point to compare the rates and the agreements and select one that is a convenient account of the available financial plan.

- Consult a Financial Advisor: It is recommended to consult a financial advisor for clarification on which of the options is most suitable for you. They can assist you in seeing how the assumption of more debt will be in the context of your financial prognosis.

FAQs

- What is equity access, and how can it help with home makeovers?

Equity access refers to leveraging the equity in your home through options like home equity loans or home equity lines of credit (HELOCs). This allows you to borrow against the value of your home to fund renovations, upgrades, or other home improvement projects.

- How long does it take to access funds through equity access?

The timeline can vary but typically ranges from a few weeks to a month, depending on the lender’s process and documentation requirements.

- Can I use equity access for other purposes besides home improvements?

Yes, you can use funds from equity access for various purposes, including debt consolidation, education expenses, or even investing in other properties.