REAL ESTATE

Achieve Your Home Makeover Dreams with Equity Access

Improving the looks of your house and making minor or major changes to your house is always very satisfying but entails a lot of expenditure. Perhaps you have always wanted to give your home a facelift but you are worried about the cost; home equity could be the answer.

Borrowing money against the value of your home allows homeowners to facilitate the renovation of their homes without the pressure that comes with expensive services. Now, let’s consider ways of realizing your home makeover visions with equity access and contemplating the varieties of financing.

Understanding Home Equity

Before going any further in explaining the home equity mortgages and loans it is important to establish the concept of home equity. Home equity can therefore be defined as the current value of your home minus the amount that is owed on the mortgage.

It is that part of your property that you can consider yours since you maintain full control over it. For instance, your home is worth $400,000, while your mortgage balance is $ 250,000; thus, your home equity is $ 150,000.

In 2023, the average Idaho HELOC balance grew 2.7% to $42,139, and more than $20 billion was added to the total HELOC debt across all U.S. consumers. This means that people in Idaho support HELOC to have a home for themselves and family.

This equity is a part of Idaho heloc and may then be utilized, especially as security for getting loans or lines of credit to finance home improvements, debt management, or any other large costs. Home equity can be tapped in three major ways and these include; the home equity mortgage, home equity loan, and the home equity line of credit or HELOC.

What is a Home Equity Mortgage?

A home equity mortgage, which is essentially a second mortgage, enables a homeowner to borrow money against the value of his/her home. This kind of credit operates in the same way as regular credit and is commonly an additional credit to the primary mortgage.

Money acquired through a home equity mortgage, among other things, can be used for home remodeling, children’s education, or paying off debts.

Advantages of a Home Equity Mortgage

- Lower Interest Rates: The benefit of home equity is often the lower interest rate than in the case of a personal loan or credit card since the mortgage is secured by the house.

- Tax Benefits: Often the interest given on a home equity mortgage is tax deductible, so it is a cheap source of funding.

- Flexible Use of Funds: You are free to spend the money you get from the home equity mortgage on anything you want to, as the money is yours.

Disadvantages of a Home Equity Mortgage

- Risk of Foreclosure: If one defaults in paying for the home equity mortgage, the home that he offered as a security can be repossessed.

- Additional Debt: This form of credit increases the level of indebtedness that you have to manage together with your first mortgage on a home.

Home Equity Loan vs. Mortgage

As for the further decision-making process about home equity tapping, you may encounter a home equity loan vs. mortgage dilemma. As much as these two materials appear to be almost similar, they have a few distinctions to make.

Home Equity Loan

A home equity loan is a non-recourse loan in the form of a lump sum that has to be paid off in the set time with agreed monthly installments. Also known as a second mortgage, it should not be confused with a home equity mortgage though it is equally a mortgage.

Mortgage

A conventional mortgage is financing to acquire a home, and it is the foremost lien on the home in most cases. A mortgage is a type of financial scheme in which an amount is lent for purchasing a home and is repaid gradually for a specified number of years like 15, 20, and 30 years, and the home acts as security for the loan.

Comparing the Two

- Purpose: A home equity loan is more or a line of credit that is taken to meet specific purposes such as home improvement or payment of other expenses whilst a mortgage is intended for the purchase of a dwelling.

- Loan Amount: Home equity loans are based on the equity the home and the borrower has in the house while mortgages are taken based on the cost of the house.

- Repayment Terms: Both have a fixed date through which they are to be paid, but the length of the date may vary as well as the interest rates of each of the credit types: home equity loan and the original mortgage.

Mortgage vs. Home Equity Loan: Which is Right for You?

This paper aims to determine the suitability of taking a mortgage or a home equity loan depending on specific factors. Here are some factors to consider:

When to Choose a Home Equity Loan

- Home Improvement Projects: Whereas, if the borrower is interested in getting funds for certain home improvements, then a home equity loan will help him get a lump sum amount that will be enough for the required purpose.

- Debt Consolidation: High-interest debts can be consolidated using the home equity loan which can, in turn, allow you to pay off that particular loan at a lower interest rate.

- Fixed Payments: Fixed interest rate along with the payment schedule is also an advantage of home equity loans particularly when it comes to monthly payments.

When to Choose a Mortgage

- Home Purchase: A conventional mortgage is suitable if one is purchasing a new home.

- Lower Interest Rates: In case you get a new mortgage that attracts a lower interest rate than the one on your current mortgage, then consolidating your existing mortgage would make sense.

- Long-Term Planning: If you intend to live in your house for many years, fixed-rate mortgages which have long-term installments prove to be useful.

Home Equity Line of Credit (HELOC)

The other possibility to get your home equity is the Home Equity Line of Credit also known as HELC. A HELOC is different from a home equity loan in that a HELOC is an open line of credit that works like a credit card whereby a homeowner borrows only what he needs and up to the limit for as long as the credit is active.

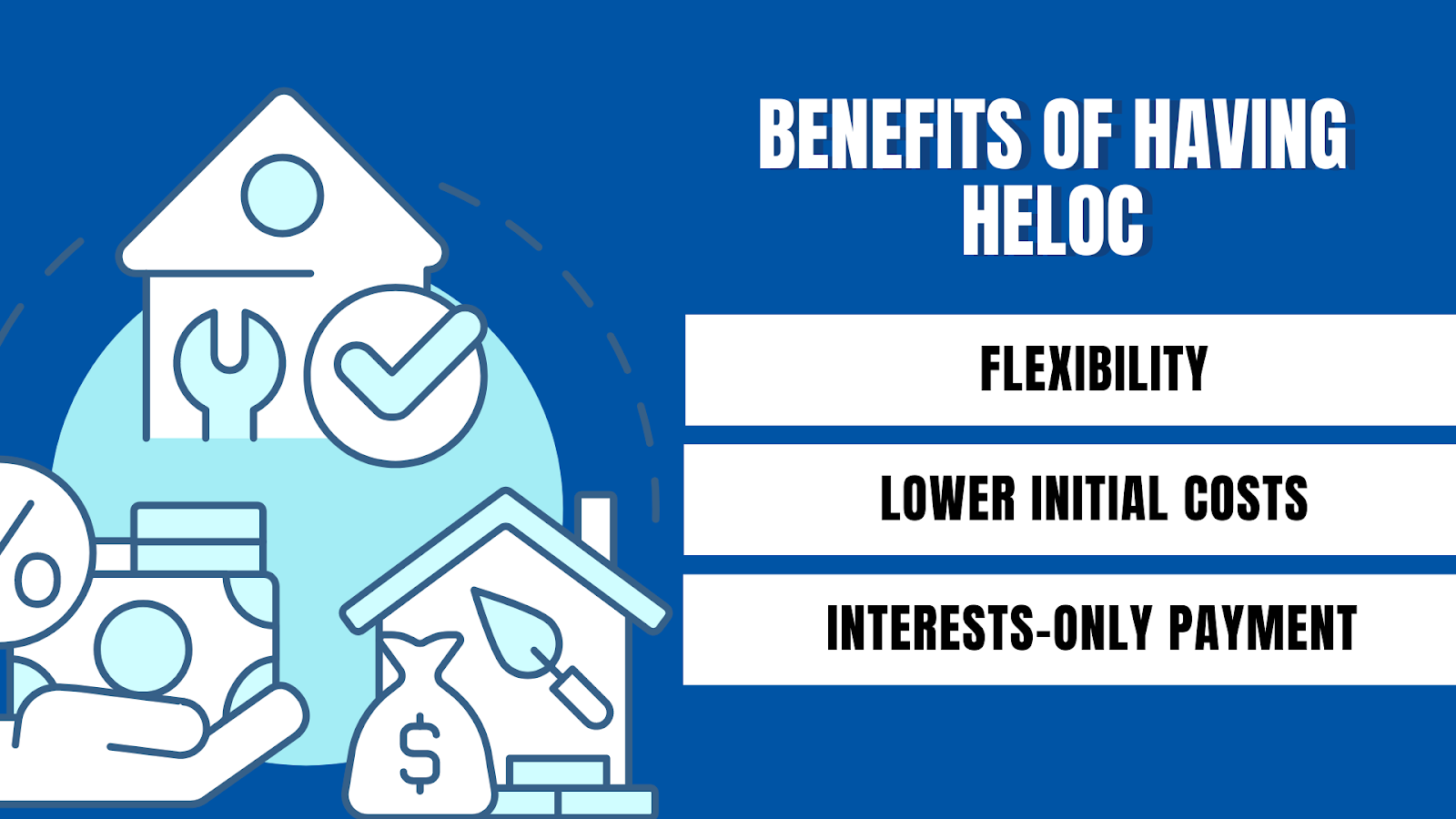

Benefits of a HELOC

- Flexibility: The amount of money you can borrow to fund is not restricted and can range from very small to very large hence suitable for projects with fluctuating costs.

- Lower Initial Costs: Specifically, one should note that HELOCs are generally cheaper in terms of the initial costs compared to home equity loans.

- Interest-Only Payments: The money is perhaps very easy to access and during the draw period, one can even start to make interest-only payments for ease of cash flow.

Drawbacks of a HELOC

- Variable Interest Rates: Some HELOCs come with variable interest rates and this, for most applicants, means that the rates cannot remain fixed.

- Potential for Overspending: This is one of the biggest drawbacks of having a HELOC because the availability of a line of credit, creates room for spending that is beyond one’s ability to pay.

- Collateral Risk: Other than these, your home is used as security, meaning that should you be unable to make your payments, your home can be repossessed.

Making the Decision

It is therefore important to factor in one’s circumstance, objective, and the construction and remodeling needs of the makeover project when deciding the applicability of the home equity mortgage, home equity loan, or home equity line of credit. Here are some steps to help guide your decision:

- Assess Your Equity: To begin with, it is recommended to know how much of an equity one has in the home. It must be noted that this is the maximum loan amount you can be approved for, the actual amount that you may be deemed to qualify for will depend on several factors that the loan officers consider when approving the loans.

- Evaluate Your Needs: Think about the range and expense of your home transformation work. Do you want to finance a large remodeling project or common repairs and improvements? It is also necessary to identify the total amount of the given and anticipated costs to compare different funding opportunities.

- Compare Interest Rates and Terms: Check and compare interest rates and all terms that concern home equity mortgages, home equity loans, and HELCOs. Make it a point to compare the rates and the agreements and select one that is a convenient account of the available financial plan.

- Consult a Financial Advisor: It is recommended to consult a financial advisor for clarification on which of the options is most suitable for you. They can assist you in seeing how the assumption of more debt will be in the context of your financial prognosis.

FAQs

- What is equity access, and how can it help with home makeovers?

Equity access refers to leveraging the equity in your home through options like home equity loans or home equity lines of credit (HELOCs). This allows you to borrow against the value of your home to fund renovations, upgrades, or other home improvement projects.

- How long does it take to access funds through equity access?

The timeline can vary but typically ranges from a few weeks to a month, depending on the lender’s process and documentation requirements.

- Can I use equity access for other purposes besides home improvements?

Yes, you can use funds from equity access for various purposes, including debt consolidation, education expenses, or even investing in other properties.

As you explore the dynamic real estate market of North Carolina, consider how crucial realtors are in navigating this complex terrain. With their finger on the pulse of both burgeoning and established markets, they’re not just agents but essential guides who enhance your investment acumen. They steer you through the intricacies of market timing and location choices, ensuring you’re poised to make well-informed decisions. Whether you’re a seasoned investor or a first-time homebuyer, understanding the role of realtors could significantly influence your strategy. What specific insights and strategies might they offer to tailor your investment decisions in North Carolina’s varied real estate landscape?

Emerging Markets in North Carolina

Within North Carolina, cities like Charlotte and Raleigh are rapidly emerging as hotspots for real estate investment, driven by robust economic growth and demographic shifts. You’ll find that urban revitalization efforts are making these areas increasingly attractive. In Charlotte, for instance, the focus on transforming historic neighborhoods into vibrant, modern hubs is reshaping the market. Economic indicators suggest a surge in both residential and commercial demand, signaling a strong return on investments here.

Raleigh, similarly, is experiencing a boom, fueled by its status as a tech and educational center. The influx of professionals and graduates is creating a demand that outstrips supply, pushing property values higher. Here, strategic investments in infrastructure and community amenities are proving to be key drivers.

Meanwhile, rural development isn’t lagging. Areas outside these urban centers are seeing growth due to improved connectivity and infrastructure. This expansion isn’t just about housing – it includes commercial properties and mixed-use developments. For you, this means diversified investment opportunities that could mitigate risks associated with urban market fluctuations.

Analyzing these trends, you’d be wise to consider how demographic changes and economic policies will continue to shape these markets. By staying informed, you can position yourself to capitalize on both urban and rural growth dynamics.

Role of Realtors in Market Dynamics

Realtors play a pivotal role in shaping the real estate markets and realtor in North Carolina, influencing both urban and rural investment trends through their strategic insights and data-driven approaches. You’ll find that their in-depth market knowledge and forecasting abilities are crucial in guiding both buyers and sellers to make informed decisions. They adeptly balance supply and demand dynamics, keeping the market fluid and responsive.

Using sophisticated data analytics, realtors identify emerging trends and opportunities. They’re not just selling homes; they’re advising on market timing, investment risks, and potential returns. This analytical approach ensures that investments are sound and timely. Realtor ethics also play a significant role here; their commitment to transparency and fairness boosts investor confidence and stabilizes the market.

Moreover, negotiation tactics employed by realtors refine the buying and selling process. They negotiate not only prices but also terms and conditions that align with their clients’ best interests. This skill set is vital in maintaining a dynamic market where values are upheld, and client satisfaction is prioritized. By mastering these tactics, realtors ensure the market remains both competitive and ethical, driving sustained investment and growth across North Carolina.

Investment Hotspots Across the State

Identifying investment hotspots across North Carolina, you’ll find strategic, data-driven insights revealing where the most promising real estate opportunities lie. Focusing on rental yields and coastal developments, let’s dive into the regions that are drawing savvy investors.

Firstly, the coastal areas of North Carolina, particularly around Wilmington and the Outer Banks, are experiencing a surge in demand. These locations not only offer high rental yields due to their popularity as vacation destinations but also present long-term appreciation prospects as the influx of new residents continues. You should consider properties that cater to both short-term vacationers and long-term residents to maximize your investment’s potential.

Moving inland, cities like Charlotte and Raleigh emerge as hotspots due to their robust economic growth and expanding job markets. The tech and finance sectors, in particular, are fueling population growth and, in turn, housing demand. Here, you might look at neighborhoods that are near major employment centers but still offer reasonable property prices, thus ensuring strong rental yields.

Analyzing historical data and future projections, it’s clear that these areas offer strategic opportunities for real estate investment. By aligning your investment strategy with these insights, you’re more likely to capitalize on the upward trends and secure substantial returns.

Strategies for First-Time Homebuyers

Navigating the real estate market as a first-time homebuyer requires a strategic approach to maximize both financial benefits and long-term satisfaction. Understanding your credit score is essential; it significantly impacts the mortgage options available to you. A higher credit score can lead to better interest rates, reducing your overall costs considerably over time. You’ll want to review your credit report meticulously, addressing any discrepancies before starting the home buying process.

Exploring various mortgage options is equally critical. Don’t just settle for the first offer you receive. Analyze different types of mortgages, such as fixed-rate, adjustable-rate, or government-backed loans like FHA, which might be more forgiving of lower credit scores and offer smaller down payments. It’s crucial to compare these based on your financial situation and long-term housing plans.

Trends in Commercial Real Estate

In recent years, the commercial real estate market in North Carolina has seen significant shifts, influenced by changing work patterns and economic factors. You’ve likely noticed the uptick in retail revitalization efforts across urban centers. This trend isn’t just cosmetic; it’s deeply strategic, tapping into consumer demand for experiential shopping that combines leisure with lifestyle. Data shows a consistent increase in foot traffic in revitalized areas, which has boosted property values and attracted a new wave of tenants keen on leveraging these bustling locales.

Industrial leases, on the other hand, are experiencing a different kind of evolution. With the rise of e-commerce, there’s been a surge in demand for warehouse spaces. This isn’t just about more square footage. It’s about strategically located properties that can support faster supply chains. As you look at the industrial lease data, you’ll see hotspots emerging near major transportation hubs. These areas are goldmines for savvy investors and businesses looking to optimize logistics and reduce delivery times to meet consumer expectations.

This analytical approach helps you understand where the market’s headed and where you should focus your investments or business strategies. Keep these trends in mind as you navigate North Carolina’s dynamic commercial real estate landscape.

Future Outlook for North Carolina Property

As you assess the future outlook for North Carolina property, remember that strategic locations and evolving economic patterns strongly influence market trajectories. You’ll find that the state’s anticipated population growth impact factors heavily into real estate valuations. With urban centers like Charlotte and Raleigh predicted to experience significant demographic shifts, there’s a direct correlation to enhanced property demand in these areas.

Economic forecasts indicate that North Carolina’s GDP is poised for robust growth, fueled by expansions in the tech and biotech sectors. This economic dynamism translates to a bullish outlook for both residential and commercial real estate markets. As employment opportunities burgeon, so does the influx of skilled workers seeking housing, thereby driving up property values and rental rates.

You should also consider the ripple effects of infrastructure developments and public policy changes. Upcoming transportation projects, for instance, are likely to boost property values in previously underconnected locales. Furthermore, any shifts in zoning laws or property taxes will be pivotal in shaping investment strategies.In strategic terms, positioning yourself now in emerging hotspots or areas slated for future development could yield significant returns. Monitoring these trends and aligning your investment portfolio accordingly isn’t just advisable; it’s essential to capitalize on North Carolina’s evolving real estate landscape.

Selling a home with a tax lien can be a challenging and stressful process for homeowners. A tax lien is a legal claim by the government against your property due to unpaid taxes, and it can complicate the sale of your home. However, with the right approach and understanding of your options, you can successfully navigate this situation and sell your Connecticut home efficiently. Here’s a guide to help you understand your options and take the necessary steps to sell your home with a tax lien.

1. Understand the Implications of a Tax Lien

Before you can effectively sell your home, it’s important to understand the implications of a tax lien. A tax lien must be resolved before the sale can proceed, as it encumbers the property and signals to potential buyers that there are unpaid debts associated with it. This lien can affect your credit score and complicate the transfer of the property’s title.

2. Determine the Amount Owed

The first step in dealing with a tax lien is to determine the exact amount owed. Contact the local tax authority or visit their website to find out the total amount due, including any interest and penalties. Having a clear understanding of your financial obligation will help you make informed decisions about how to proceed with the sale.

3. Explore Your Payment Options

There are several ways to address a tax lien, and your choice will depend on your financial situation and the specifics of your lien.

- Pay the Lien in Full: If you have the financial means, paying off the lien in full is the most straightforward solution. Once the lien is satisfied, you can proceed with selling your home without any encumbrances.

- Set Up a Payment Plan: If paying the lien in full is not feasible, you may be able to negotiate a payment plan with the tax authority. This arrangement allows you to make regular payments over time, but keep in mind that the lien will remain on the property until it is fully paid off.

- Seek a Lien Release: In some cases, you may be able to negotiate a partial payment or settlement with the tax authority in exchange for a lien release. This would allow the sale to proceed, with the remaining balance potentially being paid from the sale proceeds.

4. Selling the Property with the Lien in Place

If you’re unable to pay off the lien before selling, you can still sell your property, but the lien must be addressed during the sale process.

- Negotiate with Buyers: Be upfront with potential buyers about the tax lien. Some buyers, particularly real estate investors, may be willing to purchase the property and assume responsibility for resolving the lien. This may result in a lower sale price, but it allows you to proceed with the sale.

- Use the Sale Proceeds to Pay the Lien: If your property has sufficient equity, you can use the proceeds from the sale to pay off the lien at closing. This requires coordination with the escrow agent or closing attorney to ensure that the lien is satisfied from the sale proceeds before any remaining funds are disbursed to you.

5. Work with a Real Estate Agent Experienced in Distressed Sales

Navigating the sale of a property with a tax lien can be complex, and working with a real estate agent experienced in distressed sales can be invaluable. An experienced agent can help you understand your options, market your property effectively, and negotiate with buyers and the tax authority. They can also assist in coordinating the sale process to ensure that the lien is properly addressed at closing.

6. Consider a Short Sale

If your property’s market value is less than the amount owed on the mortgage and the tax lien, a short sale may be an option. In a short sale, the lender agrees to accept less than the total amount owed on the mortgage, and the tax authority may agree to release the lien in exchange for a portion of the sale proceeds. This process can be complex and time-consuming, requiring approval from both the lender and the tax authority, but it can provide a way to sell the property and resolve the lien.

7. Consult with a Tax Professional or Attorney

Given the legal and financial complexities involved in selling a property with a tax lien, consulting with a tax professional or real estate attorney is highly advisable. They can provide expert guidance on your specific situation, help negotiate with the tax authority, and ensure that all legal requirements are met during the sale process.

Conclusion

Selling a Connecticut home with a tax lien presents unique challenges, but it is possible with the right approach and resources. By understanding the implications of the lien, exploring payment options, negotiating with buyers, and working with experienced professionals, you can efficiently navigate the sale process. Whether you choose to pay off the lien, negotiate a settlement, or sell the property as-is, taking proactive steps will help you achieve a successful sale and resolve your tax obligations.

Understanding the differences between leasehold and freehold properties is essential for anyone involved in buying or selling real estate in the UK. Estate agents in Shropshire explain the key differences, responsibilities, and rights associated with each type of ownership, providing valuable insights for estate agents and potential buyers.

Freehold: Complete Ownership and Control

Freehold ownership is the most absolute type of property ownership in the UK. As a freeholder, you own the property and the land on which it stands outright, without any time restrictions. This type of ownership is typical for most houses and gives the owner complete control over the property, including the responsibility for its maintenance. There are no ground rents, service charges, or any other landlord charges to worry about, which makes it a preferred option for many buyers.

Key Benefits

Full Control: The owner has total control over the property and land.

No Lease Length Concerns: Unlike leasehold, there’s no countdown on how long you own the property.

Fewer Restrictions: Fewer restrictions on what you can do with the property.

Owning a Share of Freehold

For those owning a leasehold property, acquiring a share of the freehold can be a game-changer. This typically happens when leaseholders band together to buy the freehold of the building from the existing freeholder. To initiate this, leaseholders serve a Section 13 Notice and usually set up a company to manage the building’s affairs. This arrangement gives them more control over the management of the property and can be a step towards extending the lease terms more favorably.

Key Advantages

Increased Control: Share of freehold gives leaseholders more say in how the property is managed.

Potential Lease Extension: Makes it easier to negotiate lease extensions.

Reduced Costs: Can potentially reduce costs associated with ground rents and other charges.

Commonhold Properties: A Modern Alternative

Commonhold is a relatively new approach that serves as an alternative to leasehold. In a commonhold, each unit owner owns their property outright and shares the responsibility for managing and maintaining the common parts of the property. This system does not have a lease’s time limit, providing a permanent ownership solution. Commonhold associations, formed by the owners, manage the property collectively, offering a democratic and equally shared management structure.

Benefits of Commonhold

No Expiry: Ownership does not expire as it does with leasehold terms.

Collective Management: Owners have an equal say in the management of common areas.

Transparency in Costs: Shared costs are managed transparently among the owners.

Leasehold: Understanding the Limitations

Leasehold ownership means owning a property for a fixed term but not the land on which it stands. This is common with flats and some houses, where the freeholder retains ownership of the land. Leasehold terms can vary significantly, and key considerations include the lease’s remaining term, service charges, and the potential for lease extensions. Leasehold can sometimes involve complex fee structures and obligations, which are crucial for potential buyers to understand.

Critical Considerations

Lease Duration: Shorter leases can affect property value and mortgage possibilities.

Service Charges: Costs for services, maintenance, and building insurance are shared among leaseholders.

Lease Extension: Leaseholders can negotiate extensions, but this can be costly.

Lease Extension and Charges

Leaseholders have the right to request a lease extension after two years of ownership, typically adding 90 years to the existing lease. However, the cost can vary and may need negotiation or even a tribunal. It’s important for leaseholders to be aware of the additional charges they may incur, including service charges, ground rent, and other administrative fees, which contribute to the upkeep of the property.

Key Points

Lease Extension Eligibility: Available after two years of ownership.

Potential Costs:Extension costs can be significant and vary widely.

Shared Responsibilities: Costs for repairs and maintenance are shared among leaseholders.

Management Disputes and Rights

Leaseholders are not without recourse in cases of dissatisfaction with property management. The Right to Manage allows them to take over management responsibilities, or they can appoint a new manager. These measures ensure that leaseholders are not unfairly taken advantage of and have a say in the management of their properties.

Protective Measures

Right to Manage: Allows leaseholders to assume management responsibilities.

Appointing a New Manager: Leaseholders can choose a new manager if dissatisfied with the current management.

Dispute Resolution: Legal avenues are available for resolving disputes with landlords or managing agents.

This comprehensive guide provides a foundational understanding of the different property ownership types, helping estate agents and buyers navigate the complexities of the real estate market effectively.

HOME IMPROVEMENT1 year ago

HOME IMPROVEMENT1 year agoThe Do’s and Don’ts of Renting Rubbish Bins for Your Next Renovation

- BUSINESS1 year ago

Exploring the Benefits of Commercial Printing

- HOME IMPROVEMENT10 months ago

Get Your Grout to Gleam With These Easy-To-Follow Tips

BUSINESS1 year ago

BUSINESS1 year agoBrand Visibility with Imprint Now and Custom Poly Mailers

- HEALTH10 months ago

Your Guide to Shedding Pounds in the Digital Age

- HEALTH10 months ago

The Surprising Benefits of Weight Loss Peptides You Need to Know

- TECHNOLOGY12 months ago

Dizipal 608: The Tech Revolution Redefined

HEALTH1 year ago

HEALTH1 year agoHappy Hippo Kratom Reviews: Read Before You Buy!