BUSINESS

Why Paying Minimum Credit Card Payments Increases Debt

Have you thought about why your credit card balance seems stuck, even though you’re making payments every month? The answer might surprise you. Many people fall into the trap of only making minimum payments on their credit cards, not realizing the long-term consequences.

This practice can turn a manageable debt into a financial burden that lasts for years. In this article, we explore why minimum payments are problematic, how they increase your overall debt, and what you can do to break free from this cycle.

What Is a Minimum Payment?

A minimum payment is the smallest amount that your credit card issuer will accept toward your outstanding balance in a given billing cycle. This amount is typically a percentage of your total balance, often ranging from 2% to 4%, plus interest and any fees.

Some issuers may have a fixed minimum amount, such as $25 or $35 if the percentage-based calculation falls below this threshold. The exact calculation of minimum payments can vary between credit card issuers, but a common formula includes a percentage of the balance (e.g., 1%), plus interest accrued during the billing cycle, plus any fees (like late payment fees), or a fixed amount, whichever is greater.

For example, if you have a $1,000 balance with an 18% APR, your minimum payment might be calculated as 1% of $1,000 ($10) plus monthly interest ($1,000 x 18% / 12 months = $15), totaling a $25 minimum payment.

Understanding the minimum payment is crucial, but it’s equally important to know how to settle credit card debt if you find yourself overwhelmed by accumulating balances. Settling credit card debt involves negotiating with creditors to potentially reduce the total amount owed, which can provide relief if managed correctly. This approach might be necessary when minimum payments are no longer a feasible option and you’re looking for a way to regain financial stability.

The Appeal of Low Payments

Minimum payments can seem attractive because they appear affordable in the short term. For many people with tight budgets, the option to pay just $25 or $35 per month on a credit card balance seems like a manageable way to handle their debt. This perceived affordability can lead to a false sense of financial security.

However, this apparent affordability masks the true cost of carrying a balance and making only minimum payments. The reality is, by paying only the minimum, you barely cover the interest charges, let alone make a dent in the principal balance. This approach can lead to a long-term cycle of debt that becomes increasingly difficult to break.

The Mathematics of Minimum Payments

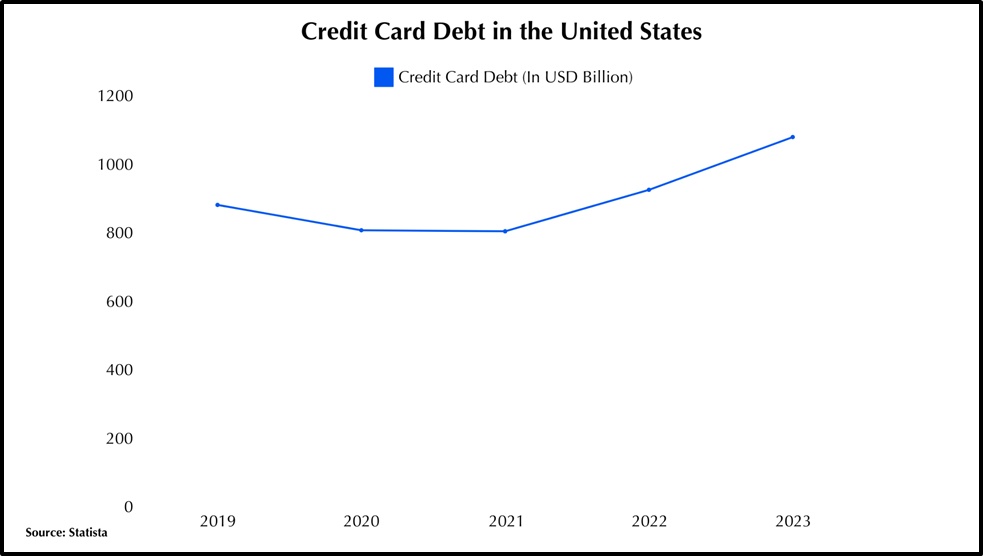

To grasp why minimum payments are problematic, consider a credit card with a $5,000 balance and 18% APR. With a minimum payment of 2% or $20, whichever is greater, the initial payment would be $100. At this rate, it would take over 34 years to pay off the debt, with a total payment of $14,423.12 – nearly triple the original balance.

The Impact of Interest

The dramatic increase in total payment is due to compound interest. Minimum payments primarily cover interest rather than reducing the principal balance. This slow balance reduction allows interest to accrue on a high balance month after month.

Over time, this compounding effect significantly increases overall debt. The result is a long-term financial burden that can take decades to overcome, illustrating the importance of paying more than the minimum whenever possible.

The Debt Spiral

Making only minimum payments can lead to a debt spiral that’s difficult to escape. As your credit card balance remains high due to minimum payments, your available credit decreases. This reduction in available credit can lower your credit score, potentially leading to higher interest rates on future loans or credit cards.

Additionally, the psychological trap of minimum payments can create a false sense of financial security. You may feel like you’re managing your debt responsibly by making regular payments, but in reality, you’re barely treading water.

This can lead to continued overspending and accumulation of debt. If the situation worsens, you might even find yourself sued for credit card debt, adding legal pressures to your financial burdens.

The long-term financial impact of this approach is significant. The money spent on interest over the years represents a substantial opportunity cost. Those funds could have been invested, saved for retirement, or used for other important financial goals. By making only minimum payments, you’re not just increasing your debt; you’re potentially sacrificing your long-term financial well-being.

Strategies to Break Free from the Minimum Payment Trap

Understanding the dangers of minimum payments is the first step; now let’s explore effective strategies to manage credit card debt more efficiently.

The most straightforward approach is to pay more than the minimum whenever possible. Even small increases can make a significant difference. For example, on a $5,000 balance at 18% APR, paying an extra $50 per month reduces the payoff time from 34 years to just under 4 years, saving over $8,000 in interest.

For those with multiple credit cards, the debt avalanche method is highly effective. This involves focusing on paying off the card with the highest interest rate first while making minimum payments on others. Once the highest-rate card is paid off, move to the next highest. This method minimizes the total interest paid across all cards.

If you have good credit, consider balance transfer options. Transferring high-interest balances to a card with a 0% introductory APR can provide breathing room to make larger payments towards the principal. Be aware of transfer fees and have a plan to pay off the balance before the introductory period ends.

Creating a budget and cutting expenses can free up additional money for credit card payments. Track your spending, identify areas to cut back, and consider ways to increase your income. Allocate any freed-up funds towards your credit card debt.

Lastly, don’t hesitate to negotiate with your credit card company. You might be able to request a lower interest rate, especially if you have a good payment history. Some issuers offer hardship programs for those facing temporary financial difficulties. Remember, the goal is to pay off your balance quickly to minimize interest and break free from the debt cycle.

| Strategy | Best For |

| Minimum Payments | Those in temporary financial difficulty |

| Fixed Higher Payments | Those who can afford to pay more |

| Debt Avalanche | Those with multiple debts |

| Debt Snowball | Those needing motivation |

| Balance Transfer | Those with good credit and a repayment plan |

The Importance of Financial Literacy

One of the reasons people fall into the minimum payment trap is a lack of understanding about how credit cards work. It’s crucial to read and understand your credit card agreement, including the Annual Percentage Rate (APR), how interest is calculated, fees associated with the card, and purchase grace periods.

Developing healthy financial habits is the key to breaking free from the cycle of debt. This includes living within your means by creating and sticking to a budget, using credit cards responsibly—ideally paying off the full balance each month—building an emergency fund to avoid relying on credit cards for unexpected expenses, and regularly reviewing your financial situation to adjust strategies as needed.

Conclusion

Managing credit card debt doesn’t have to be a struggle. By understanding the pitfalls of minimum payments and implementing smart repayment strategies, you can take control of your finances. Remember, every extra dollar you pay above the minimum makes a difference.

Start today by reviewing your credit card statements, creating a budget, and planning to pay more than just the minimum. Your future self will thank you for securing financial freedom.

Frequently Asked Questions

Are there alternatives to credit cards for emergency expenses?

Yes, alternatives include building an emergency fund, seeking personal loans from credit unions, or exploring community assistance programs for specific needs.

What’s the difference between secured and unsecured credit cards?

Secured credit cards require a cash deposit as collateral, while unsecured cards don’t. Secured cards are easier to get and can help build credit.

How often should I check my credit report?

It’s recommended to check your credit report at least once a year. You’re entitled to one free report annually from each of the three major credit bureaus.

Do I need a lawyer for credit card lawsuit?

A lawyer can be beneficial in a credit card lawsuit, especially if the debt is large or you have a valid defense. However, for small claims, you might represent yourself.

For investors seeking a blend of stability and steady income in their investment portfolios, debt income funds offer a promising avenue. Often viewed as a safer alternative to equity investments, these funds can provide regular income while preserving capital. This detailed guide delves into the world of debt income funds, helping you understand and learn opportunities with debt income funds to make informed investment decisions that align with your financial goals, learn opportunities with depb income funds

What are Debt Income Funds?

Debt income funds, commonly referred to as fixed-income securities, invest in a combination of debt instruments such as government bonds, corporate bonds, mortgage-backed securities, and other debt securities. The primary aim of these funds is to provide investors with regular income through interest payments, making them an ideal choice for income-focused investors.

Key Benefits of Investing in Debt Income Funds

1. Regular Income Stream: One of the most appealing aspects of debt income funds is their potential to generate a steady and predictable income stream through interest payments, which can be distributed monthly or quarterly to investors.

2. Lower Risk Profile: Compared to stocks and other equity investments, debt income funds typically have a lower risk profile. The investments are made in securities that have a fixed repayment schedule and interest rate, providing greater security and stability.

3. Diversification: By incorporating debt income funds into your portfolio, you can diversify your investments and reduce overall risk. This diversification can help buffer against volatility in the stock market.

4. Capital Preservation: Investors who are risk-averse or nearing retirement may find the capital preservation aspect of debts income funds attractive. These funds focus on maintaining the principal investment while providing returns through interest income.

How to Invest in Debt Income Funds

Step 1: Assess Your Financial Goals and Risk Tolerance

- Determine your investment objectives and how much risk you are willing to accept. Understanding your need for income generation versus capital growth is crucial in choosing the right debt income fund.

Step 2: Research Different Funds

- Learn opportunities with debts income funds by researching various funds available in the market. Look into their performance history, the credit quality of bonds they hold, their interest rate sensitivity, and management fees.

Step 3: Diversify Your Investments

- Consider diversifying across different types of debt funds, such as short-term, long-term, corporate bond, and government bond funds to balance risk and optimize returns.

Step 4: Monitor and Rebalance

- Regularly review your investment to ensure it continues to meet your financial goals. Rebalance your portfolio as necessary in response to changes in market conditions or in your financial circumstances.

Key Considerations When Choosing Debt Income Funds

1. Interest Rate Risk: Interest rate changes can affect the value of debts income funds. When interest rates rise, the value of existing bonds typically falls.

2. Credit Risk: The risk that the issuer of a bond will not be able to make principal and interest payments. Review the credit ratings of the bonds within the fund’s portfolio to assess this risk.

3. Inflation Risk: Inflation can erode the purchasing power of the payments from bonds. Consider inflation-protected securities as a potential component of your investment strategy.

4. Liquidity Risk: Some debts income funds may invest in securities that are less liquid than others, making it difficult to sell these investments at a fair price.

Maximizing Returns from Debt Income Funds

1. Use a Laddering Strategy: By creating a portfolio of bonds with staggered maturities, you can manage interest rate risks and provide liquidity and income continuity over time.

2. Focus on Quality: Investing in bonds with higher credit ratings may offer lower yields but provide greater security and stability.

3. Stay Informed: Keep up with financial news and trends related to interest rates and economic indicators that can impact bond markets. Knowledge can be a powerful tool in adjusting your investment strategy proactively.

Conclusion

Debt income funds can serve as a cornerstone of a well-rounded investment portfolio, offering benefits such as regular incomes, reduced risk, and capital preservation. By taking the time to learn opportunities with debt incomes funds and understanding how to effectively manage these investments, you can significantly enhance your financial stability and success. Whether you are a conservative investor focused on incomes or someone looking to diversify their investment risks, debt incomes funds provide a viable and strategic option for achieving your long-term financial objectives.

From the flick of the switch in our homes to the aggressive markets that power our industries, energy trading is an indispensable aspect of modern life. It’s a complex dance of supply and demand, regulations, geopolitics, and weather that hinges on one thing above all – information.

In this high-stakes arena, ETRM systems serve as beacons of order in an otherwise turbulent financial world. These systems are the backbone of energy trading and provide the necessary tools to manage risk.

Let’s take a closer look at how ETRM systems are unlocking growth in the energy trading industry.

Read on to begin!

Improved Operational Efficiency

This energy trading solution streamlines and automates many processes. This includes trade execution and settlement. These systems save time and resources for energy trading companies. This is made possible by reducing manual work and human error.

This allows them to focus on more strategic tasks. Such tasks include analyzing market trends and developing new trading strategies. Also, this power trading platform can integrate with other business functions. They can span from accounting and risk management.

This allows them to provide a comprehensive view of the company’s operations. Such an integration improves efficiency. This is achieved by eliminating silos and promoting better communication between departments.

Enhanced Decision-Making

Access to real-time data and advanced analytics tools is crucial in today’s fast-paced energy trading market. ETRM systems provide traders with accurate and up-to-date information on:

- market conditions

- supply and demand dynamics

- price fluctuations

This enables them to make faster, more informed decisions. Thus, allowing them to have a competitive edge.

Traders can also identify profitable opportunities and act on them before their competitors. This comes along with the ability to analyze vast amounts of data.

If you discover more about ETRM systems, you will find that some also offer predictive analytics. They help forecast future market trends and optimize trading strategies with the right decisions. This can further enhance a company’s bottom line.

Moreover, ETRM systems can also be tailored to fit the unique needs and processes of each energy trading company. This ensures that they are adaptable to different market conditions and regulations.

Scalability and Adaptability

ETRM systems must also be able to adapt and scale accordingly. This comes along as the energy trading industry continues to evolve. Such systems are designed to handle large volumes of data. Thus, they can easily integrate with new technologies and platforms.

This scalability allows energy trading companies to grow their operations. This is also achieved without worrying about outgrowing their systems. It enables them to quickly respond to market changes. Thus, adopt new trading strategies as needed.

Explore the Benefits of ETRM Systems in Energy Trading

ETRM systems play a crucial role in the energy trading industry. These systems are essential for navigating the complex and dynamic landscape of energy trading. They help unlock growth opportunities for companies.

The use of ETRM systems will only increase in importance. This comes along as technology continues to advance and regulations become more stringent.

So, embracing these systems if you are looking to succeed in the energy trading market.

Should you wish to explore other topics, visit our blog page. We’ve got more posts!

Introduction to Fill Dirt

In the realm of construction, landscaping, and environmental projects, the term “fill dirt” often emerges as a critical component. This humble material serves as the foundation for various endeavors, offering support, stability, and a plethora of other benefits. In this article, we delve into the depths of fill dirt, exploring its definition, uses, types, benefits, challenges, and much more.

What is Fill Dirt?

Definition

Fill dirt san Diego, in its simplest form, refers to the soil used to fill in depressions, level off terrain, or raise the ground’s elevation. It typically consists of soil excavated from construction sites or agricultural areas.

Composition

Fill dirt is primarily composed of soil, clay, sand, gravel, and organic matter. Its composition can vary depending on the source and location, with different ratios of these components influencing its properties.

Uses of Fill Dirt

Fill dirt finds widespread applications across various industries:

Construction

In construction projects, fill dirt is indispensable for creating a solid foundation, leveling building sites, and backfilling trenches or excavations.

Landscaping

Landscapers utilize fill dirt to sculpt the terrain, fill in low-lying areas, and create raised beds or slopes for gardens and outdoor spaces.

Environmental Projects

Fill dirt plays a crucial role in environmental restoration efforts, such as wetland mitigation, erosion control, and reclamation of disturbed sites.

Types of Fill Dirts

Several types of fill dirt are commonly used:

Topsoil

Topsoil is the uppermost layer of soil, rich in organic matter and nutrients, making it ideal for gardening and landscaping projects.

Subsoil

Subsoil lies beneath the topsoil and consists of clay, silt, and sand. While less fertile than topsoil, it provides structural support and stability.

Organic Fill

Organic fill, derived from compost or decomposed plant matter, enhances soil fertility and drainage, making it suitable for agricultural and landscaping purposes.

Benefits of Using Fill Dirts

Cost-Effectiveness

Fill dirt is often readily available at construction sites or excavation projects, reducing the need for purchasing expensive materials.

Stability and Support

Fill dirts provides a stable foundation for structures, prevents soil erosion, and minimizes the risk of foundation settlement.

Environmental Benefits

Using fill dirts from local sources reduces the environmental impact associated with transporting soil over long distances, thereby lowering carbon emissions.

How to Choose Fill Dirt

Selecting the right fill dirt is crucial for the success of any project:

Quality Assessment

Inspect the fill dirts for debris, contaminants, and proper soil composition to ensure its suitability for the intended use.

Quantity Estimation

Calculate the volume of fill dirts required based on the project’s specifications and dimensions of the area to be filled.

Source Verification

Verify the source of fill dirts to ensure compliance with local regulations and avoid potential legal issues or environmental liabilities.

Preparing and Using Fill Dirt

Proper preparation and installation techniques are essential for maximizing the benefits of fill dirt:

Site Preparation

Clear the area of vegetation, debris, and any obstructions before spreading fill dirts to ensure a smooth and even surface.

Proper Installation Techniques

Compact the fill dirts in layers using heavy machinery to achieve the desired density and stability, preventing future settlement.

Safety Considerations

While fill dirts offers numerous advantages, it also poses certain risks that must be addressed:

Environmental Impact

Improper disposal or contamination of fill dirts can harm ecosystems, pollute water sources, and disrupt natural habitats.

Soil Testing

Conduct soil tests to assess the quality and composition of fill dirts, identifying any potential contaminants or hazardous substances.

Erosion Control

Implement erosion control measures such as silt fences, vegetation barriers, and sediment ponds to prevent soil erosion and runoff.

Challenges Associated with Fill Dirt

Despite its utility, fill dirts presents certain challenges that require careful consideration:

Contamination Risks

Fill dirts sourced from industrial sites or landfills may contain pollutants, toxins, or hazardous materials that pose health and environmental risks.

Settlement Issues

Improper compaction or inadequate site preparation can lead to settlement problems, structural damage, and costly repairs.

Regulatory Compliance

Complying with local regulations, permits, and environmental standards is essential when sourcing and using fill dirts to avoid legal repercussions.

Case Studies and Examples

Explore real-world examples of fill dirts projects, highlighting successful implementations, innovative techniques, and lessons learned.

Future Trends in Fill Dirt Usage

As technology advances and environmental concerns grow, the use of sustainable fill materials, such as recycled aggregates and synthetic soils, is expected to rise.

Conclusion

In conclusion, fill dirt serves as a versatile and invaluable resource in various industries, offering solutions for construction, landscaping, and environmental challenges. By understanding its properties, applications, and considerations, stakeholders can harness the full potential of fill dirts while mitigating risks and maximizing benefits.

FAQs

What is the cost of fill dirt?

- The cost of fill dirts varies depending on factors such as location, quantity, and quality. It can range from a few dollars per cubic yard to higher prices for specialty blends or certified soil.

Can fill dirts be used for gardening?

- Fill dirts can be used for gardening, but its suitability depends on the composition and quality of the soil. Mixing fill dirt with compost or topsoil can improve its fertility and drainage for gardening purposes.

How do I know if the fill dirts is suitable for my project?

- Conduct a thorough inspection and testing of the fill dirts to assess its composition, compaction, and potential contaminants. Consulting with soil experts or engineers can also provide valuable insights into its suitability for specific projects.

Is fill dirts the same as topsoil?

- Fill dirts and topsoil are distinct types of soil with different compositions and uses. While topsoil is rich in organic matter and nutrients, fill dirts is often composed of subsoil, clay, sand, or recycled materials and is primarily used for filling and grading purposes in construction and landscaping projects.

Are there any environmental concerns associated with fill dirts?

Fill dirts sourced from contaminated sites or containing hazardous materials can pose environmental risks, including soil and water pollution, habitat destruction, and health hazards. Proper testing, sourcing, and disposal practices are essential for minimizing these concerns.

ENTERTAINMENT1 week ago

ENTERTAINMENT1 week agoExploring the Kristen Archives: A Treasure Trove of Erotica and More

TECHNOLOGY4 months ago

TECHNOLOGY4 months agoBlog Arcy Art: Where Architecture Meets Art

- LIFESTYLE1 week ago

Who Is Sandra Orlow?

- LIFESTYLE4 months ago

The Disciplinary Wives Club: Spanking for Love, Not Punishment

- ENTERTAINMENT5 days ago

Kiss KH: The Streaming Platform Redefining Digital Engagement and Cultural Currents

- GENERAL4 months ago

What are stories of male chastity? A Comprehensive Guide

- ENTERTAINMENT4 weeks ago

MonkeyGG2: Your Personal Gaming Hub

- GENERAL5 months ago

SmartSchoolBoy9: The Rise of a Viral Chasing Kid Sensation